Behind Noida Airport’s Tariff Order: Airlines, Regulators and a High-Stakes Aviation Gamble

- Noida International Airport’s tariff order highlights the growing strain within India’s airport privatisation model, where regulators are balancing private infrastructure recovery, airline economics and ambitious traffic growth expectations.

- Airlines including Air India and IndiGo questioned whether traffic can shift from Delhi to Jewar at the projected pace, citing concerns around dual-airport operations, route ramp-up and Delhi airport’s continued ability to absorb growth.

- While AERA moderated some cost assumptions and deferred part of the airport’s revenue recovery, the final order largely preserves YIAPL’s capital recovery framework, leaving unresolved whether airlines can profitably build scale at Jewar quickly enough.

Buried beneath the 382 pages of the Airports Economic Regulatory Authority (AERA) of India’s latest tariff order for Noida International Airport is a far more consequential story than a mere fixation of landing charges and passenger fees.

What emerges instead is an unusually candid portrait of the growing structural tensions within India’s airport privatisation regime itself—a regime in which regulators are increasingly being forced to reconcile three fundamentally incompatible objectives: allowing private airport developers to recover massive upfront infrastructure investments, keeping airline operating economics viable in an intensely price-sensitive market, and simultaneously projecting greenfield airports as engines of future traffic growth capable of rivalling established metropolitan hubs.

The tariff order for Noida International Airport (DXN), issued on May 12 for the first control period between FY27 and FY31, effectively institutionalises this contradiction rather than resolving it.

On paper, the regulator has attempted moderation. The Airports Economic Regulatory Authority (AERA) trimmed portions of Yamuna International Airport Pvt. Ltd.’s (YIAPL) traffic assumptions, reduced certain operational cost benchmarks, capped salary escalations, deferred recovery of nearly ₹800 crore into the next control period, and acknowledged—sometimes explicitly—that the concerns raised by airlines regarding traffic uncertainty, cost escalation, and dual-airport competition were not without merit.

Yet despite these concessions, the core structure of the tariff framework remains unmistakably tilted toward preserving the financial viability of the concessionaire rather than reducing the economic burden on airlines attempting to build operations at a greenfield airport whose commercial success remains far from assured.

That underlying bias becomes evident from the final numbers themselves.

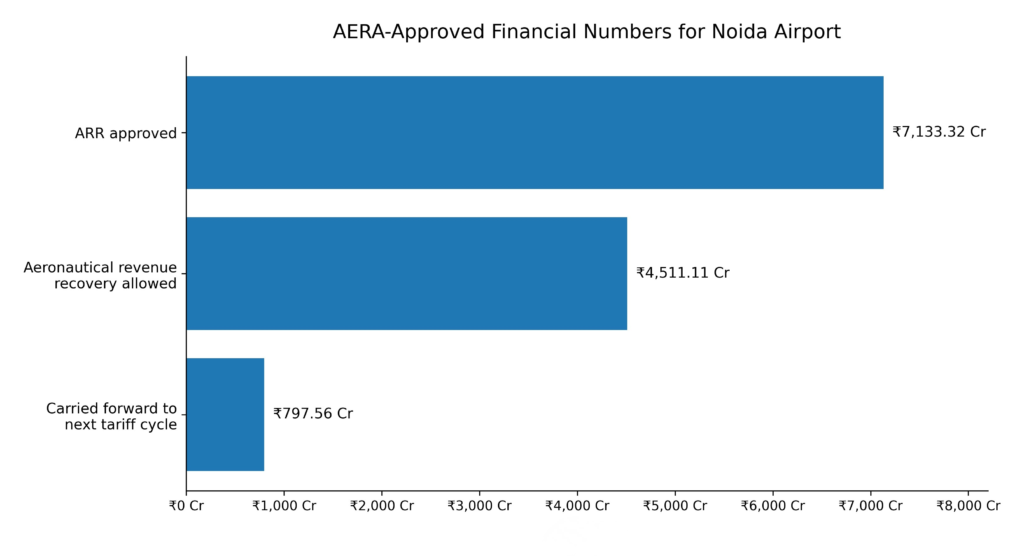

AERA has approved an Aggregate Revenue Requirement (ARR) of ₹7,133.32 crore and allowed YIAPL to recover ₹4,511.11 crore in aeronautical revenues during the first control period, while carrying forward another ₹797.56 crore into the subsequent tariff cycle.

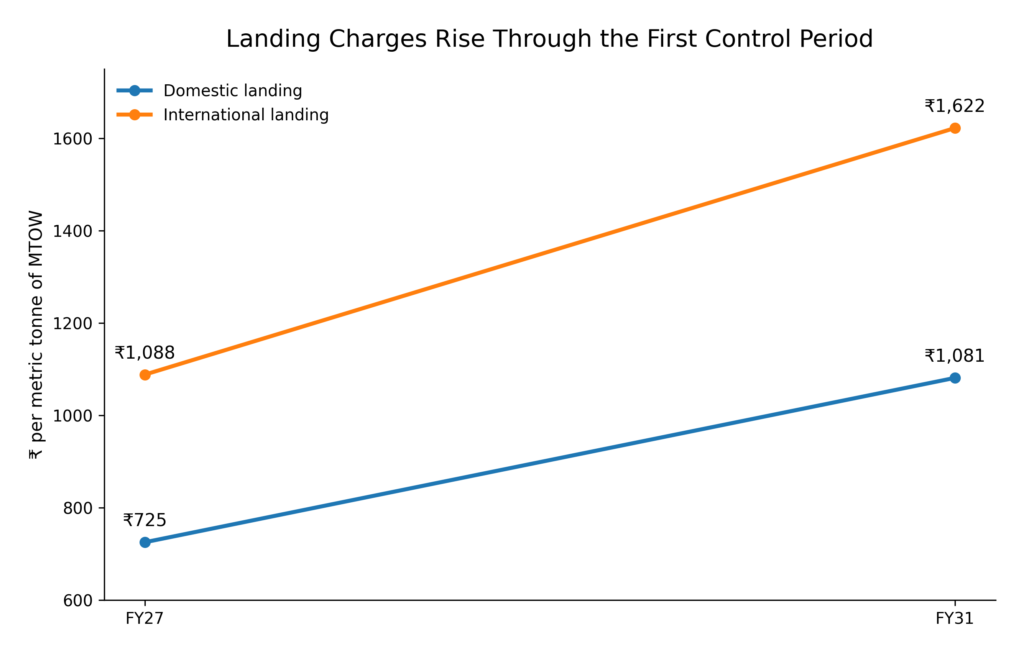

Domestic landing charges will begin at ₹725 per metric tonne of Maximum Take-Off Weight (MTOW) in FY27 and rise steadily to ₹1,081 by FY31, while international landing charges escalate from ₹1,088 to ₹1,622 per MT during the same period.

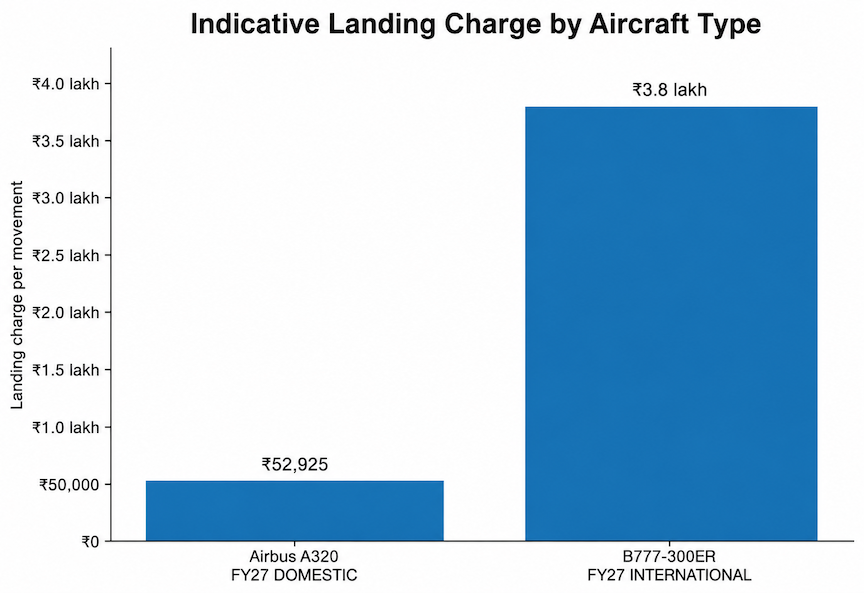

A narrow-body Airbus A320 aircraft will pay roughly ₹52,925 in landing charges during the initial year alone, while a Boeing 777-300ER operating an international flight could face landing charges approaching ₹3.8 lakh before parking, navigation, ground handling, CNS/ATM, and passenger-related costs are even factored in.

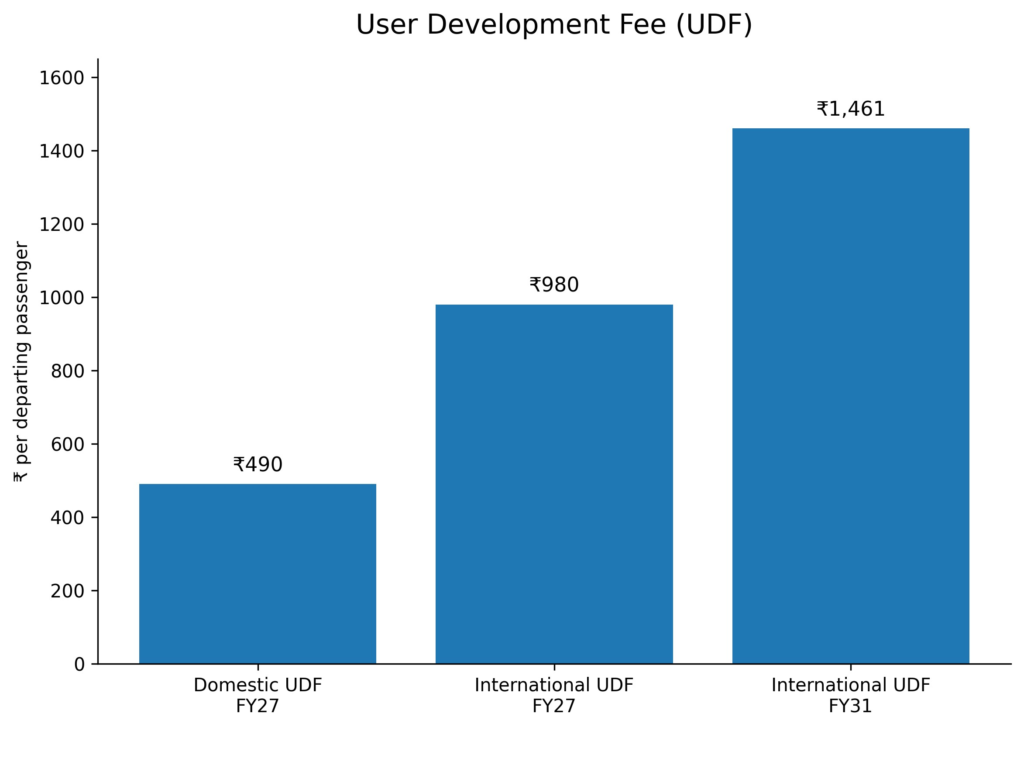

Simultaneously, domestic departing passengers will pay a User Development Fee (UDF) of ₹490 and international passengers ₹980 in the first year, with those charges climbing sharply through the control period.

By FY31, international embarking passengers will pay ₹1,461 merely in UDF. In practical terms, this means that even before airlines begin pricing fuel, crew, aircraft ownership, maintenance, or network costs into their ticket structures, the airport itself will already have imposed a substantial economic layer onto route viability.

It is precisely this front-loading of cost recovery that triggered such aggressive resistance from airlines and international aviation bodies during the consultation process.

The most revealing aspect of the proceedings, however, was not simply that airlines objected—that is routine in tariff determinations—but the extent to which the objections exposed deep scepticism about the assumptions underpinning India’s newest mega-airport projects.

The battle over traffic forecasts, in particular, became less a technical dispute and more a referendum on whether regulators and airport operators are systematically overestimating the pace at which airlines can realistically migrate traffic away from established hubs such as Delhi’s Indira Gandhi International Airport.

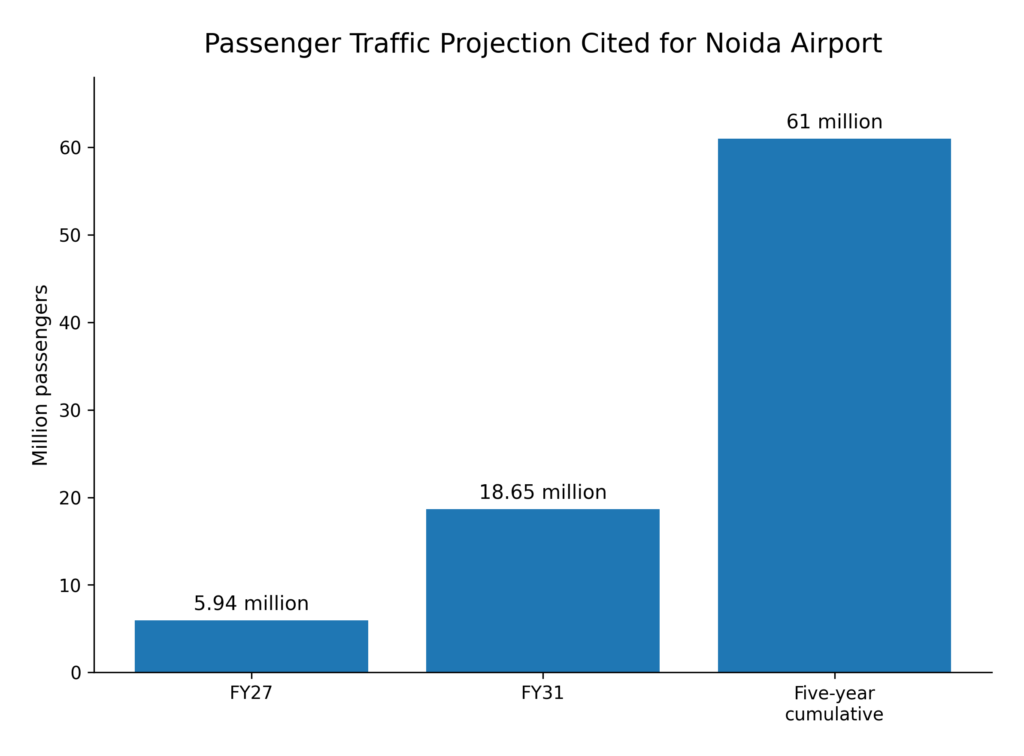

YIAPL’s own consultant, Landrum & Brown, projected passenger traffic growing from 5.94 million passengers in FY27 to 18.65 million by FY31, implying cumulative traffic of roughly 61 million passengers over five years.

AERA initially revised these assumptions upward during the consultation phase, effectively assuming that delays in the commencement of operations would create pent-up demand capable of accelerating traffic growth once the airport opens.

What followed was a remarkable inversion of the usual regulatory dynamic: the airport operator itself objected to the regulator being too optimistic.

YIAPL warned that AERA’s assumptions regarding accelerated post-delay demand lacked grounding in airline discussions and regional capacity conditions. Airlines, meanwhile, attacked the projections from an entirely different angle, arguing not merely that the forecasts were optimistic, but that the entire underlying logic of traffic diversion from Delhi airport remained commercially fragile.

Air India argued that the projections underestimated the competitive resilience of Delhi airport, whose own ongoing expansion—including terminal enhancements and international capacity additions—could continue absorbing growth that DXN hopes to capture. More importantly, Air India questioned whether premium-yield business traffic, which remains essential for airline profitability, would willingly migrate to Jewar without dramatically superior connectivity infrastructure.

The airline’s comparison with Navi Mumbai International Airport was particularly telling, because it implicitly highlighted a growing fear among carriers that India’s next generation of greenfield airports may replicate a familiar pattern: ambitious infrastructure creation followed by prolonged struggles to build economically sustainable traffic density.

Photo: IndiGo

IndiGo, while somewhat less confrontational in tone, nevertheless challenged the aggressive pace of projected growth during the initial years and warned that route ramp-up at a new airport is rarely linear, particularly when airlines themselves remain constrained by aircraft delivery delays, network optimisation pressures, and the economics of maintaining split operations across dual-airport systems.

The intervention by the International Air Transport Association (IATA) was arguably even more consequential because it moved beyond operational objections into the philosophical architecture of India’s airport regulation itself.

IATA’s argument regarding “risk asymmetry” struck at the heart of the regulatory model: namely, that airport operators are effectively protected from downside traffic risk because under-recoveries can be compensated through future tariff revisions, whereas airlines—which bear the immediate commercial consequences of weak passenger demand—possess no comparable recovery mechanism.

In essence, IATA was arguing that the regulatory framework socialises airport risk while privatising airline risk.

AERA rejected that argument firmly, insisting that airports themselves remain exposed because infrastructure costs are fixed and cannot be flexibly adjusted in the manner airlines alter capacity or redeploy aircraft. Yet the regulator’s own order simultaneously demonstrates the structural imbalance airlines were pointing toward.

Even after acknowledging traffic uncertainty, moderating passenger assumptions, and carrying forward ₹797.56 crore into the next control period specifically to avoid “adversely impacting passenger traffic growth,” AERA still preserved the overwhelming majority of YIAPL’s capital recovery framework.

That contradiction becomes sharper when examining the regulator’s treatment of individual cost items.

Lufthansa Group mounted one of the most detailed attacks on YIAPL’s operational and capital assumptions, challenging cargo forecasts, salary structures, manpower escalation, maintenance expenditure, and the inclusion of several assets within the Regulatory Asset Base (RAB).

Lufthansa argued that personnel costs benchmarked at ₹0.21 crore per employee remained excessive for a greenfield airport and warned that allowing such salary structures would institutionalise inflated cost bases from inception. Although AERA partially agreed by reducing YIAPL’s original proposal from ₹0.25 crore and capping annual escalation at 6% instead of 10%, it ultimately rejected Lufthansa’s demand for deeper benchmarking aligned with more efficient airports such as Hyderabad and Ahmedabad.

Similarly revealing was the dispute over CNS/ATM charges, where both Lufthansa and IATA objected to the 30% overhead loading attached to the Airport Authority of India (AAI) cost recoveries.

In an unusually blunt acknowledgement, AERA itself admitted that the overhead lacked a “clear and demonstrable linkage” to actual service provision. Yet despite recognising the weakness of the justification, the regulator retained the overhead structure in the final order anyway, effectively conceding the airlines’ criticism while simultaneously refusing to act upon it.

That pattern repeated across multiple areas of dispute. Airlines challenged the inclusion of the boundary wall, VVIP terminal, body scanners, baggage systems, and various security infrastructure within the aeronautical asset base, arguing that airlines and passengers were being compelled to fund expenditures only tangentially related to core passenger operations.

AERA rejected virtually all such objections, consistently prioritising the interpretation that any asset linked even indirectly to airport functionality qualified for recovery through aeronautical charges.

Even YIAPL, despite emerging as the broader beneficiary of the order, failed to secure several major demands. The airport operator’s attempt to obtain a higher Fair Rate of Return through an Indian Institute of Management Ahmedabad-backed argument for a “greenfield premium” was rejected decisively by AERA, which refused to differentiate DXN from existing brownfield airports despite the project’s substantially different risk profile.

Likewise, YIAPL’s push for higher inflation assumptions tied to crude oil volatility and Middle East geopolitical risks found little regulatory sympathy.

Ultimately, the order reveals a regulator attempting to preserve equilibrium within a deeply imbalanced system.

AERA clearly recognises that excessively high charges risk suppressing traffic growth at DXN during precisely the years when network formation is most critical.

Yet the regulator also appears unwilling—perhaps institutionally unable—to fundamentally challenge the underlying financial architecture of India’s airport concession model, which depends on allowing private operators predictable long-term cost recovery on massive infrastructure investments.

The unresolved question, therefore, is no longer whether Noida International Airport or the viability of a greenfield private airport can be built. It is whether airlines can profitably build scale there quickly enough to justify the assumptions embedded within the very tariff structure designed to finance it.

That answer will not emerge from another consultation paper or regulatory order. It will emerge from passenger behaviour, airline network economics, and the uncomfortable possibility—one the airlines hinted at repeatedly throughout the proceedings—that India’s aviation infrastructure ambitions may now be expanding faster than the market’s ability to absorb their costs.

* R Suryamurthy has been an economic analyst and journalist for more than three decades and has worked for The Telegraph, Tribune and Press Trust of India.

Also Read: Safran: Advancing Hybrid-Electric Propulsion for the Next Generation