- Adani Airport Holdings Limited (AAHL) has partnered with MakeMyTrip to move duty-free sales into the trip-planning stage, targeting travellers before they reach the airport and expanding pre-order access across its network.

- Despite rising passenger traffic, airport retail continues to see low conversion, with most travellers not buying, and a significant share of duty-free spend shifting to overseas hubs such as Dubai and Singapore.

- With India’s non-aero revenue per passenger still far below global benchmarks, Adani is building a multi-channel digital distribution model to capture more of that spend within Indian airports.

When Dubai Duty Free announced its 2025 results at the start of the year, the figure was staggering even by its own history—USD 2.38 billion in annual sales across Dubai International and Al Maktoum airports, a record for the retailer’s 42-year history, achieved over 10 consecutive record-breaking months.

That works out to roughly USD 25 per international passenger at an airport handling about 95 million travellers a year.

European airport duty-free sales rose 5.5%. year-on-year to €10.13 billion, though average spend per passenger stagnated at €10.55, reflecting a ‘decoupling’ where traffic growth is outpacing retail conversion, a trend Adani is trying to avoid in India.

India’s private PPP airports, including Mumbai and Delhi, were generating USD 4.3 per passenger from all non-aero revenue in FY24, against London Heathrow at USD 19.8 per passenger and Singapore Changi at USD 18.1 per passenger, with a global range of USD 8 to USD 20 per passenger, according to the ratings agency ICRA. Within non-aero, duty-free is the single largest and highest-margin component, making India’s specific gap in airport retail yield wider still.

That disparity in non-aero yield, and specifically in duty-free conversion, is what Adani Airport Holdings Limited (AAHL) is working to close, and the partnership it announced with MakeMyTrip is its latest attempt to do so.

Outbound Traffic, Offshore Revenue

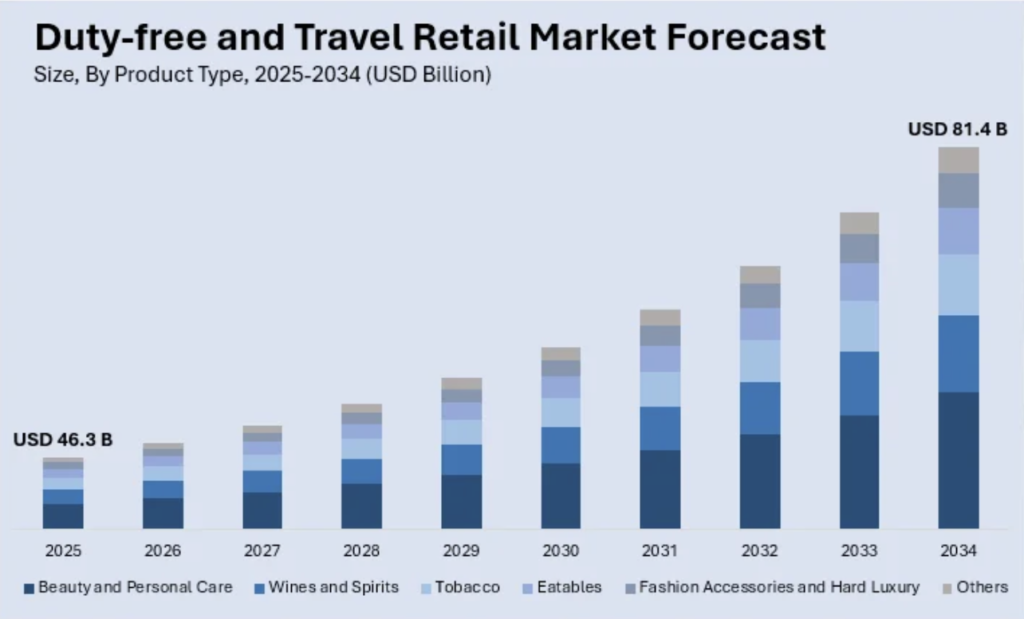

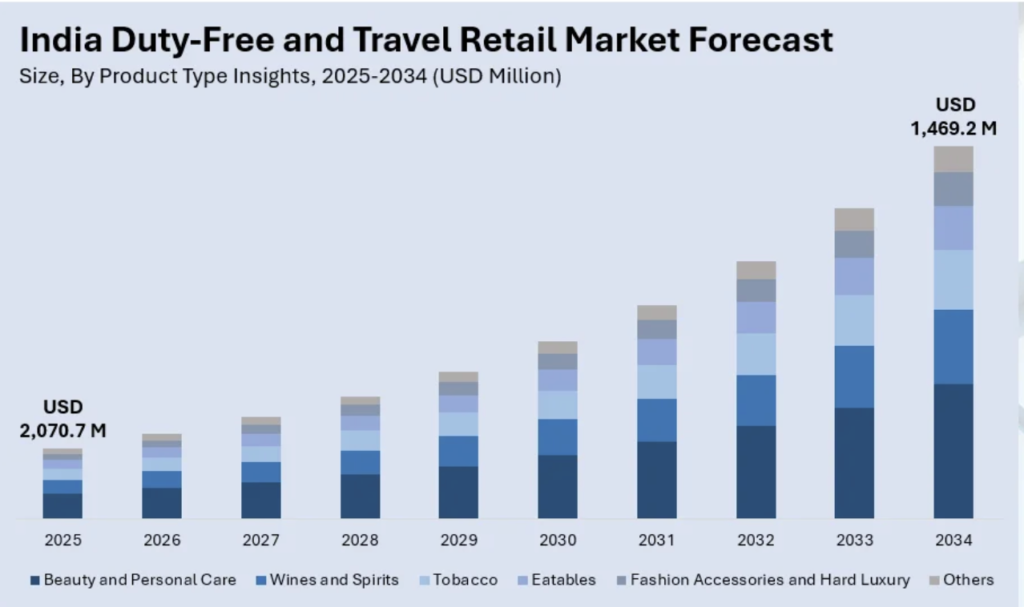

The statistical contrast is stark. Dubai Duty Free’s USD 2.38 billion in 2025 sales exceeded the estimated size of India’s entire duty-free and travel-retail market, which IMARC Group puts at USD 1.47 billion for the same, growing at a compound annual rate of 3.69 per cent toward a projected USD 2.07 billion by 2034.

The entire Gulf Cooperation Council (GCC) duty-free retail market is estimated at over USD 6.5 billion in 2025, with Dubai Duty Free alone accounting for USD 2.38 billion, roughly 36% of the regional total.

India is among the largest sources of outbound travel to the UAE, with 3.27 crore Indians having travelled abroad in 2025, a record, with the UAE, Saudi Arabia and Thailand as the top three destinations.

A meaningful share of the duty-free spend that these travellers generate flows into Dubai International and Abu Dhabi rather than into Indian airports on the way out or back in.

Singapore’s Changi Airport, another transit hub where Indian passengers stop frequently, has built a concession model studied by airport operators worldwide, blending in-terminal retail with pre-order services that extend well beyond the physical store.

The practical result is that Indian airports are losing duty-free revenue at both ends of the journey: outbound passengers spend at Dubai or Singapore, and returning passengers have already bought what they wanted before coming home.

High Footfall, Low Conversion

The problem is not product range or pricing. Kearney‘s 2024 large-scale travel retail study found that 95 per cent of Indian shoppers say duty-free pricing is attractive to them, and 83 per cent say airport retail offerings have improved, particularly in locally relevant and gift-worthy categories.

Yet only five to ten per cent of travellers at airport duty-free stores globally actually buy anything, compared with conversion rates of 40 to 60 per cent in shopping malls carrying comparable products, and Kearney found that 64 per cent of those who walk past a duty-free store express dissatisfaction with either pricing transparency or assortment.

What India buys at duty-free also tells its own story. Airport duty-free liquor in India generated USD 536 million in 2024, with the segment growing at 11.4 per cent a year and projected to cross USD 1.02 billion by 2030.

Four in five Indian travellers who enter a duty-free store head straight to the liquor section, making it the primary driver of footfall.

Yet in terms of revenue share, perfume and cosmetics are the largest category in India’s duty-free market, with electronics and gifts now the fastest-growing segment, according to IMARC—a composition that reflects an aspirational, gift-focused shopper whose purchasing decision is susceptible to prior influence rather than an impulse buy at the gate.

A passenger who has already decided at home to buy a bottle of single malt or a specific perfume is significantly more likely to follow through than one relying on a quick scan of the shelves under time pressure between check-in and boarding.

Adani Pushes Duty-Free Into the Booking Flow

International travellers flying through AAHL’s duty-free outlets at Mumbai, Ahmedabad, Lucknow, Mangaluru, Jaipur and Thiruvananthapuram can now pre-book duty-free on MakeMyTrip’s app or mobile web, for both departure and arrival journeys, with pick-up at the airport store and access to pricing available exclusively through the pre-order channel.

The MakeMyTrip platform offers access to over 14,000 SKUs across more than 10 product categories and 100 brands, enabling travellers to pre-book ahead of their journey through MakeMyTrip’s app and mobile web. The integration extends the purchase decision into the initial trip-planning stage.

Arrival pre-booking works differently. Most returning Indian travellers complete their duty-free purchases at an overseas airport, such as Dubai, Singapore or London, because the purchase window is in front of them on the outward leg, and by the time they are heading home, they have already spent.

Adani’s arrival pre-order shifts that decision earlier: a traveller who plans and reserves online before leaving India can collect at an Indian airport on return, moving a transaction that would otherwise have completed at a foreign terminal into AAHL’s network instead.

The MakeMyTrip partnership is the third significant digital channel AAHL has added to its duty-free business in roughly twelve months, and each of the three targets a distinct point in the traveller’s booking and planning journey.

In 2024, Adani Digital Labs tied up with EaseMyTrip to embed duty-free pre-ordering into EaseMyTrip’s airport services booking flow, making AAHL’s digital storefront accessible to travellers already on EaseMyTrip’s platform, who could choose ancillaries alongside their ticket.

In March 2026, AAHL and IndiGo launched a loyalty programme that gives IndiGo BluChip members 5 points for every ₹100 spent on pre-booked duty-free purchases at Adani airports, with the scheme active at the same six airports and plans to extend it to Guwahati and Navi Mumbai.

IndiGo carried 124 million passengers in 2025, the first Indian airline to cross that number in a single year, and holds approximately 64 per cent of India’s domestic market. AAHL’s pre-order catalogue is now embedded in the carrier’s booking journey, which moves more than six in every ten passengers flying within India.

On international routes, it overtook the Air India Group to become India’s largest international carrier by passenger count in the second half of 2025, making the BluChip scheme directly relevant to the outbound international flyer that duty-free pre-order is designed to reach.

MakeMyTrip adds a different dimension due to its dominance, particularly in international travel booking. The company reported gross bookings of approximately USD 9.8 billion in FY2025, with international travel contributing around a quarter of total revenue and international air ticketing accounting for an all-time high share of 38 to 42 per cent of air ticketing revenue, a share that has grown consistently as outbound Indian travel has expanded.

With over 87 million lifetime transacted users, a presence in more than 150 countries, and recent expansions into the UAE and Saudi Arabia, the platform is where a large proportion of India’s outbound and inbound international trips are planned and confirmed.

For a duty-free pre-order service whose commercial logic depends entirely on reaching the traveller before they leave home, MakeMyTrip’s position in the international booking funnel is what makes this partnership different from the earlier EaseMyTrip and IndiGo arrangements.

With IndiGo and two major online travel agency (OTA) platforms now in AAHL’s duty-free distribution structure, the most notable absence is Air India. Together, IndiGo and Air India Group account for about 91 per cent of India’s domestic aviation market.

Air India’s international network spans long-haul routes to the United Kingdom, North America, Europe and the Gulf, and its passengers, particularly in business and premium-economy cabins on those routes, represent the traveller segment with both the inclination and the purchasing power to spend in the higher-value duty-free categories: premium spirits, cosmetics and luxury goods, the segments that generate the most revenue per transaction globally.

The Tata Group’s Tata Neu platform cross-sells flights, hotels and retail benefits through a single app, positioning it as a competing travel-and-lifestyle interface rather than an obvious partner channel.

Whether Adani seeks a formal duty-free integration with Air India similar to the IndiGo BluChips arrangement, or accepts that OTA reach through MakeMyTrip and Goibibo is sufficient to capture Air India passengers who book through those platforms, regardless of the airline’s own digital ambitions, neither company has disclosed a position on this. The commercial logic for closing that gap is clear enough, regardless.

Global Playbooks Already Exist

The pre-order model has an established track record in markets that adopted these digital strategies earlier than India, and the evidence from those implementations is instructive. Dallas/Fort Worth International launched a duty-free pre-order with 3Sixty Duty Free and Grab in January 2021 to improve queue management and surface a wider product range than any physical store could display. The service was explicitly designed to extend the ‘dwell time’ digitally, allowing passengers to consider purchases rather than making rushed decisions airside.

Delhi Airport‘s own duty-free operator introduced click-and-collect in the same period—an experiment that began as a pandemic-era convenience but evolved into a permanent high-engagement channel.

Similarly, Virgin Atlantic’s Retail Therapy and EVA Air’s SKY SHOP allow passengers to select items from a full digital inventory at home for collection onboard or at the airport. These services rely on the premise that a deliberate purchase from a comprehensive range carries a higher transaction value than a high-pressure impulse buy from a limited gate display.

Dubai Duty Free, whose 2025 sales grew by 9.85 per cent year-on-year—outpacing passenger traffic by an estimated 5 per cent—attributes this performance to strategies that successfully decoupled retail growth from mere footfall. By focusing on penetration and transaction value, they have created a model that digital pre-order is now designed to replicate in the Indian context.

The consistent finding across Dallas, Singapore, Dubai, and Europe’s major hubs is that duty-free success is no longer a function of terminal dwell-time alone. Instead, it relies on a digital relationship that begins well before the passenger arrives at the airport. India’s airports, despite their record-breaking passenger growth, are only just beginning to operationalize this pre-terminal engagement at scale.

India’s broader travel retail market, encompassing all airport and transit retail categories beyond pure duty-free, generated USD 3.68 billion in 2024, according to Grand View Research, and is forecast to reach USD 7.18 billion by 2030, with an annual growth rate approaching 12 per cent.

Kearney’s India-specific modelling, somewhat more conservative in its assumptions, puts India’s travel retail at nearly USD 1 billion by 2030 on a base-case CAGR of 7.3 per cent, with India’s outbound travel market set to grow at 14.27 per cent a year through to 2030, with the number of outbound trips expected to exceed 50 million before the end of this decade.

Those numbers matter to Adani because AAHL holds the duty-free concession in full at Mumbai through its wholly owned subsidiary, Mumbai Travel Retail Private Limited, with Flemingo Travel Retail as the JV partner at the remaining six airports.

This means every additional rupee of pre-order revenue across the network flows back into the group’s own concession structure rather than to an outside operator. Mumbai alone handled approximately 16.3 million international passengers out of a total 55.5 million in calendar year 2025.

Asia-Pacific is the largest regional market in global duty-free and travel retail, according to IMARC, driven by outbound travel from China, India and Southeast Asia, yet India’s per-passenger duty-free yield remains a fraction of what Singapore and Dubai generate from travellers who, in many cases, are Indian.

The gap between India’s current non-aero yield of USD 4.3 per passenger at PPP airports, of which duty-free is only a part, and Dubai’s implied USD 25 per passenger from duty-free is not something that digital pre-order alone will close.

But it is the most direct intervention available without building more floor space, and the three distribution partnerships AAHL has secured in twelve months—with an OTA, an airline loyalty programme and now India’s dominant international travel platform- represent a more systematic attempt to address the conversion problem than anything the country’s private airport sector has tried before.

Whether that effort moves India’s duty-free yield meaningfully toward global benchmarks will be visible in AAHL’s non-aero revenue numbers over the next two to three years, and those numbers will say something not just about duty-free, but about whether Indian airports can finally capture the spending power of travellers.

What This Unlocks Next

If pre-order conversion at the six airports starts moving meaningfully above the current baseline, Adani has a fairly visible set of follow-on moves that international operators have already tested.

Using booking data—route, cabin class, trip frequency, destination—to personalise offers rather than serve a generic catalogue is the next logical step, and the data that MakeMyTrip and IndiGo hold about their international travellers gives AAHL a targeting capability that traditional airport retail has never had access to.

Beyond duty-free specifically, the same pre-booking infrastructure can accommodate lounge access, fast-track security, parking, and food and beverage vouchers, all of which are currently captured mostly through in-terminal walk-ins and yield lower per-passenger revenue than they would if they were available and marketed during the booking flow.

The Air India question resolves over time, either through a commercial arrangement between AAHL and the Tata Group or through the OTA channel. Whether Adani pushes for a direct loyalty integration with Air India similar to the IndiGo BluChips arrangement, or whether it accepts that OTA reach is sufficient, will say something about how aggressively the group wants to close the gap across India’s near-duopoly aviation market before a more competitive landscape emerges.

India’s outbound travel base is on track to reach 50 million departures before the end of this decade. Adani’s bet is that the larger that number gets, the more its network of digital pre-order channels, rather than physical store square footage, determines how much of that traffic becomes duty-free revenue.

Also Read: Closing the Conversion Gap: IndiGo–Adani’s Airport Retail Play