India’s Aviation Boom Meets a Profit Crunch as Global Turbulence Hits Earnings

- Indian airlines face a difficult FY2027 as ICRA expects industry losses to widen to ₹36,000-38,000 crore despite strong passenger demand.

- Higher fuel prices, rupee depreciation, rising lease costs and airspace disruptions are putting heavy pressure on airline margins.

- Domestic traffic remains strong, with May 2026 passenger load factors at nearly 89%, but higher costs are preventing growth from turning into stronger profits.

India’s airlines are heading into one of their most challenging financial years since the pandemic, with strong passenger demand proving insufficient to offset an unprecedented surge in operating costs driven by geopolitical tensions, elevated fuel prices and a weakening rupee.

The country’s aviation industry, long celebrated as one of the world’s fastest-growing markets, is increasingly confronting an uncomfortable paradox: aircraft are flying fuller, fleets are expanding, and passenger numbers continue to rise, yet profitability is steadily deteriorating.

Fresh assessments by ICRA and Crisil Ratings suggest FY2027 could become a defining year for Indian aviation, exposing the fragility of an industry whose balance sheets remain highly vulnerable to global shocks despite robust domestic demand.

ICRA has already lowered its domestic passenger traffic growth forecast for FY2027 to 3-6 per cent from an earlier 6-8 per cent, while slashing its international traffic growth projection for Indian carriers to 0-3 per cent from 8-10 per cent. More significantly, it now expects the industry’s net losses to widen to ₹ 36,000-38,000 crore, overturning earlier expectations of a sharp recovery.

Crisil Ratings, meanwhile, projects that the aggregate operating profit of domestic airlines will decline by 10-15 per cent in FY2027 to ₹16,000-17,000 crore, compared with around ₹19,000 crore in the previous fiscal.

Together, the reports underscore a growing reality: the biggest threat to Indian aviation is no longer demand but the economics of sustaining growth.

The financial squeeze has been triggered largely by the conflict in West Asia, which has disrupted global energy markets, increased flying distances through restricted airspace and pushed up insurance, maintenance and leasing costs.

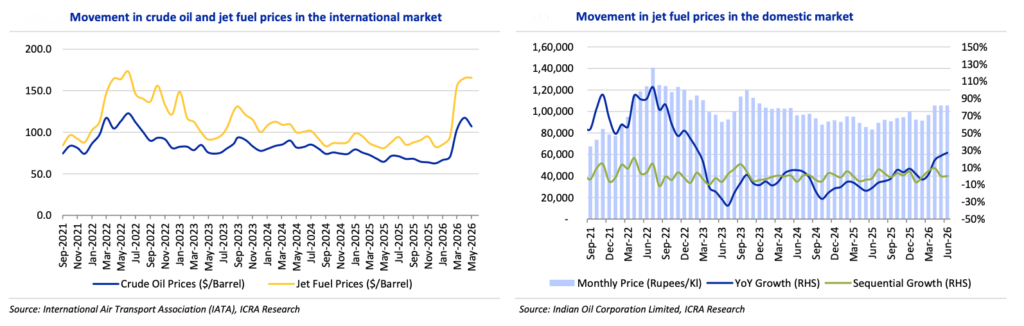

Global aviation turbine fuel (ATF) prices surged by more than 50 per cent following the outbreak of the conflict. Although prices have retreated from nearly $145 per barrel in early June to below $125 per barrel, they remain substantially above the FY2026 average of around $90 per barrel.

With fuel accounting for 40-50 per cent of airline operating costs, even a modest increase has an outsized impact on profitability.

“The surge in global fuel prices following the onset of the conflict has increased the operating cost of airlines significantly. Even with the expected moderation in fuel prices, they will remain above the levels of the last fiscal,” said Manish Gupta, Deputy Chief Ratings Officer at Crisil Ratings.

According to Gupta, the combination of elevated fuel prices and currency depreciation is expected to push the industry’s cost per available seat kilometre (CASK), excluding forex, to ₹4.8-5.0 per km in FY2027 from ₹4.3 per km last fiscal, placing sustained pressure on airline margins.

His assessment reinforces a key concern highlighted across the sector—that airlines are facing structural cost inflation rather than a temporary spike in expenses.

Indian carriers have attempted to offset rising costs by imposing fuel surcharges and adjusting fares.

Crisil estimates that revenue per available seat kilometre (RASK) will increase to ₹5.2-5.4 per km this fiscal from ₹4.9 per km last year.

However, the improvement is unlikely to fully compensate for higher costs because India’s aviation market remains intensely price-sensitive.

Airlines have limited ability to raise fares without hurting discretionary travel demand, particularly at a time when inflation is already weighing on household spending.

As a result, the gap between revenue and operating costs is narrowing even as passenger numbers remain healthy.

The industry’s aggressive fleet expansion is adding another layer of financial stress.

Indian airlines are expected to induct 90-100 aircraft during FY2027, reflecting confidence in long-term demand and the need to replace ageing aircraft.

Yet every new aircraft also brings higher lease obligations.

“Domestic airlines are facing cost pressures while pursuing significant fleet expansion, with 90-100 aircraft expected to be added this fiscal, partly for replacement and partly for expansion,” said Gautam Shahi, Senior Director at Crisil Ratings. “The upshot will be a nearly 15 per cent increase in rental costs to Rs 27,000-28,000 crore this fiscal. Along with lower operating profitability, this can weaken coverage of lease service obligations.”

While Shahi believes operating efficiencies should gradually improve over the medium term, he cautioned that airlines will need strong financial backing to navigate the current turbulence.

He said support from airline promoters, liquidity buffers, availability of credit under ECLGS 5.0, and the Government’s recently launched ATF Price Stabilisation Fund should help carriers absorb the near-term financial shock.

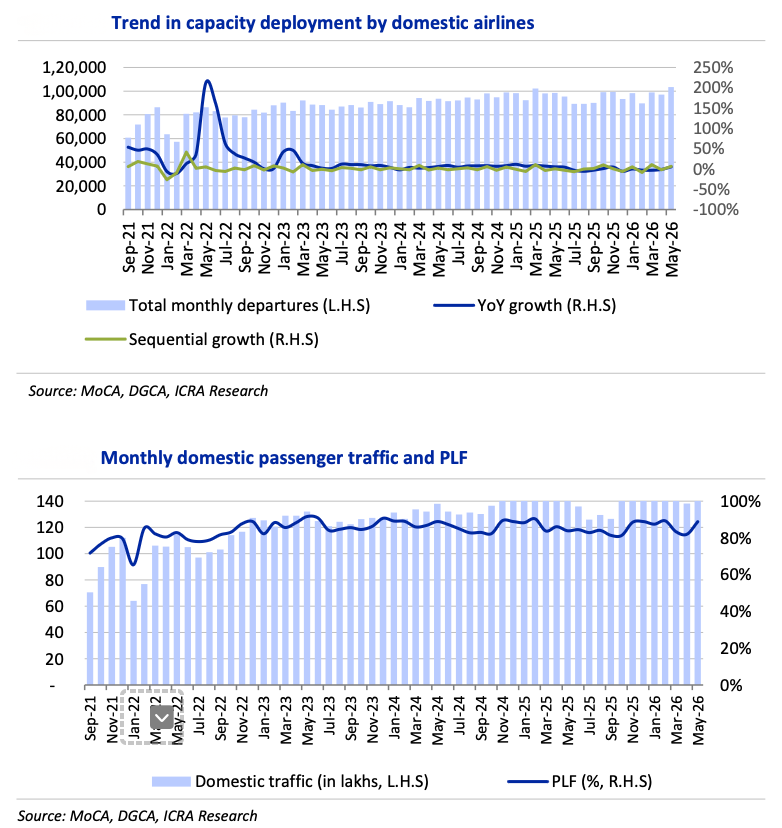

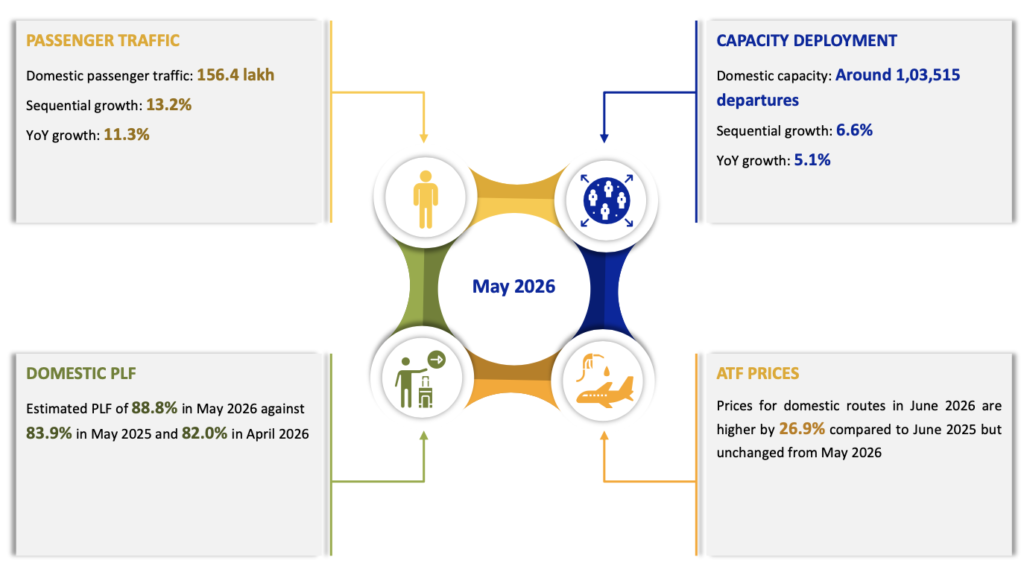

Ironically, operational indicators continue to paint a picture of resilience. ICRA estimates domestic passenger traffic reached 156.4 lakh in May 2026, up 11.3 per cent year-on-year, while passenger load factors climbed to an estimated 88.8 per cent, indicating airlines are filling nearly nine out of every ten seats. Capacity deployment also increased 5.1 per cent compared with a year earlier.

But these encouraging numbers conceal a deeper problem. The strong traffic growth was partly aided by a weak base after travel demand was disrupted by the Pahalgam terror attack and the India-Pakistan military conflict in May last year. More importantly, higher traffic is no longer translating into stronger earnings because every additional passenger is being offset by higher fuel, lease and foreign exchange costs.

The latest forecasts also underline a structural vulnerability in India’s aviation sector. Despite becoming the world’s third-largest domestic aviation market, airline profitability continues to depend heavily on variables outside the industry’s control—oil prices, geopolitical conflicts, exchange-rate movements and global aircraft supply chains.

That dependence means airlines can execute operationally almost flawlessly yet still struggle financially. If tensions in West Asia ease and crude prices continue to moderate, the industry could see some relief in the second half of FY2027. But if airspace disruptions persist or oil prices rebound, India’s airlines may find themselves trapped in a cycle where passenger traffic continues to grow while profitability continues to decline.

For an industry that has built its global reputation on rapid expansion, FY2027 may ultimately become the year that demonstrates a more sobering reality: growth without sustainable margins is not a durable business model.