- Duty-free alone may not be enough to close India’s airport non-aero revenue gap.

- Digital pre-orders can support sales growth, but retail execution and passenger dwell time will ultimately drive non-aero revenue growth.

- Premium F&B, lounge monetisation, arrivals duty-free and higher passenger spending are becoming more important airport revenue drivers.

As private operators commit billions to airport infrastructure across India’s booming aviation market, the financial viability of these expanding airport networks has steadily decoupled from sheer passenger volumes. Traditional aeronautical revenue streams remain tightly capped by regulatory pricing frameworks, while concession payouts and capital expenditure commitments continue to rise.

Long-term profitability now depends far more on what passengers spend inside the terminal, where operators must rapidly transform highly price-elastic, low-spending domestic passengers into premium retail consumers to close a widening non-aeronautical revenue deficit.

The Numbers That Matter

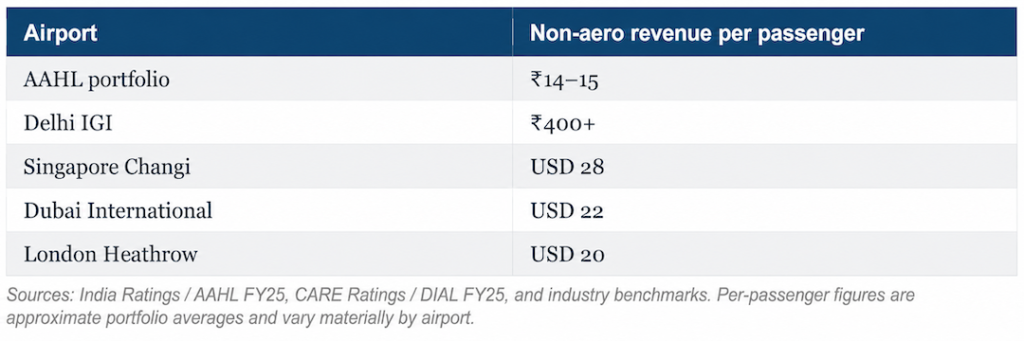

The Adani partnerships have expanded digital reach and pre-order access, but the wider airport revenue gap remains unresolved. Adani Airport Holdings (AAHL) generated approximately ₹1,359 crore in non-aeronautical revenue in FY25 across its airport portfolio, handling about 94 million passengers.

That translates to roughly ₹14 to ₹15 per passenger. Delhi’s Indira Gandhi International Airport, India’s strongest commercial performer, generated ₹3,301 crore in non-aeronautical revenue in the same year across roughly 79 million passengers, or about ₹418 per passenger. Global leaders remain higher still.

The gap between AAHL and Delhi is not a matter of a few rupees per passenger. On a total non-aeronautical revenue-per-passenger basis, Delhi is roughly 25 times ahead, which better captures the scale of the commercial challenge.

Platforms Cannot Solve Structural Constraints

In March 2026, IndiGo and AAHL linked India’s dominant airline loyalty programme to duty-free pre-orders across AAHL airports, and in April 2026, MakeMyTrip was embedded into the same catalogue, offering more than 14,000 products to travellers during booking.

These partnerships matter, but they are demand-capture tools, not substitutes for retail execution or traffic structure. Platforms can only amplify existing strengths. They cannot compensate for weak retail execution or limited international traffic.

Why Duty-Free Alone Cannot Close the Gap

Of AAHL’s 94 million passengers in FY25, the majority were domestic travellers who are not eligible for duty-free shopping.

Airports such as Ahmedabad, Lucknow, and Jaipur have limited international traffic, so duty-free can only be a partial revenue lever in a portfolio built around domestic connectivity.

Guwahati illustrates the point clearly. In FY25, it handled approximately 6.57 million passengers, including around 91,594 international passengers—meaningful in absolute terms, but still too small to make duty-free the core commercial answer.

This is not a critique of strategy. India’s aviation growth story is primarily domestic, and AAHL sits at the center of it. The point is simply that closing the revenue gap will require more than duty-free, even if duty-free becomes more efficient.

The Better Domestic Playbook

The alternative path is already visible in airports that have solved parts of this problem.

Bengaluru’s Kempegowda International Airport has built one of India’s stronger non-aero revenue profiles through premium food and beverage, lounge monetisation, and a commercially stronger domestic passenger mix.

Tokyo Haneda shows that a domestically dominant airport can still generate strong retail and F&B performance through category curation, premium positioning, and high conversion rates.

The lesson is simple: domestic passengers spend when the offer is relevant and the airport design gives them time to do it.

The NRI and Gulf Opportunity

At Mumbai, Mangaluru, and Thiruvananthapuram, international traffic is the commercial engine. Gulf-linked NRI travellers often arrive with specific purchase intent, especially for liquor, electronics, and gold. Well-executed arrivals duty-free can outperform today’s yields, but the current constraint is not demand alone. It is also floor space, pre-order capability, and execution depth.

The revised ₹75,000 duty-free allowance under the Baggage Rules 2026 is a genuine tailwind. Gulf-NRI travellers are digitally active, community-networked, and responsive to WhatsApp-based and Malayalam-language channels.

A tailored Adani One pre-order journey for this segment requires no heavy infrastructure investment and could unlock incremental revenue quickly.

Ospree: The Execution Risk

Adani’s plan to scale Ospree from 50 stores in 2025 to 310 by 2026 is strategically coherent. Vertical integration can shift margin from concessionaires to the airport operator and improve category control, data capture, and customer experience design. But rapid integration also carries a financial risk that deserves to be stated plainly.

Operators who have attempted similar transitions internationally typically experienced 12 to 18 months of revenue pressure during the changeover.

For AAHL, even a conservative shortfall of 15 to 20 per cent across the transitioning store network during that window represents hundreds of crores in foregone non-aeronautical margin at precisely the moment the portfolio needs non-aero revenue to grow fastest.

Standard best practice is to retain top-performing concessionaires as joint venture partners during the build phase rather than exiting all third-party relationships at once, and to hire experienced category managers from organisations like Dufry, Lagardère, or SSP who understand product mix, minimum guarantee negotiation, and conversion at an operational level.

The Cost Burden That Makes Execution Non-Negotiable

AAHL must raise non-aeronautical revenue from roughly ₹14 to ₹15 per passenger today toward ₹35 to ₹40 by FY28—or face serious financial strain under the combined weight of PPF obligations and active debt service.

Adani won all six PPF concession airports with bids well above competitors.

At Mangaluru, with approximately 2.32 million passengers handled in FY25 per ACI data, the annual PPF obligation is approximately ₹27 crore before a single rupee of operating revenue is recognised. These are fixed obligations paid to AAI regardless of profitability.

Layered on top is the USD 750 million in international financing secured in June 2025. With several airport SPVs still recording negative PAT, accelerated non-aero growth is not optional if AAHL wants to keep funding commercial upgrades while servicing obligations.

The group is targeting an IPO and demerger window between 2027 and 2030. The execution gap must close well before then.

What Success Looks Like by 2028

The destination is clear. Non-aeronautical revenue should move toward ₹35 to ₹40 per passenger across the portfolio.

Positive PAT should become standard across airport SPVs. NRI-heavy airports such as Mangaluru and Thiruvananthapuram should deliver stronger arrivals duty-free performance. Domestic-heavy airports such as Ahmedabad, Lucknow, and Jaipur should monetise lounges, premium F&B, and digital pre-orders more effectively.

And AAHL should be positioned not as a commercial outlier but as a reference point for what domestic-dominant airport portfolios can achieve when the operational model matures.

The Three Levers

Segmentation is the first. The Gulf-returnee NRI at Mangaluru, the first-time domestic flyer at Lucknow, the outbound business traveller at Mumbai, and the heritage tourist at Jaipur all have different triggers, price sensitivities, and time windows. Category mix, store layout, and digital prompts should reflect those differences rather than apply a uniform approach across a highly varied portfolio.

Dwell time engineering is the second, and the most under-discussed. Pre-order helps only the passengers who plan ahead. The bigger commercial opportunity lies in making sure airside time is long enough and well-designed enough to convert walk-in demand.

At Changi, security and immigration processing are designed around maximising time in the commercial zone, and the airport tracks the direct revenue correlation between dwell minutes and spend per passenger.

Indian airports need to make that same commercial case internally, with their own revenue data, to operations and infrastructure teams.

Retail execution at the point of sale is the third. Digital intent does not automatically become a transaction.

The team on the floor, their product knowledge, and their selling discipline are what close the sale. That capability is built through people, process, and time—not partnerships alone.

The Verdict

India’s airport commercial story is real. Passenger growth, regulatory improvements, and platform ambition are all genuine. But execution, not platforms, will decide whether AAHL closes the gap.

The distance between ₹14 to ₹15 per passenger today and ₹35 to ₹40 by FY28 is not a technology problem. It is a retail operation, category management, and passenger-experience problem.

And given the financial obligations underneath the portfolio, time is the one variable AAHL cannot afford to waste.

*About the Author – Ashraf Fathi has 25 years of experience in airport commercial strategy, duty-free operations, and concession management across MENA and Africa. He served as Managing Director of Dufry Group (now Avolta) in Egypt and Kenya, and advises airport operators and governments on commercial performance and retail strategy. This article reflects independent analysis based on publicly available industry data and benchmarks.

Also Read: Adani’s Digital Push to Reclaim India’s Duty-Free Spend