- Regional aviation demand in India already exists, but growth will depend on shifting short-haul travel from road and rail to air through affordable, frequent services.

- Turboprops are structurally better suited to this shift, as their economics align with short sectors, lower risk, and sustained frequency between tier-2 and tier-3 cities.

- Global experience shows that regional connectivity works when aircraft choice matches network realities, making turboprops central to India’s next phase of regional aviation growth.

For years, India’s regional aviation discussion has revolved around demand creation, policy incentives, and airport development. Increasingly, however, the debate is narrowing to a more fundamental question: What kind of aircraft economics can actually make short-haul regional flying work at scale?

The answer is aircraft choice.

As India’s domestic market matures beyond metro trunks, growth is shifting toward shorter sectors linking tier-2 and tier-3 cities. These are routes where frequency matters more than size, affordability matters more than speed, and commercial risk has to be carefully managed. In that operating environment, turboprops are not simply one option among many; they are the aircraft category most closely aligned with the structural realities of regional connectivity.

Regional demand already exists—aviation’s share does not

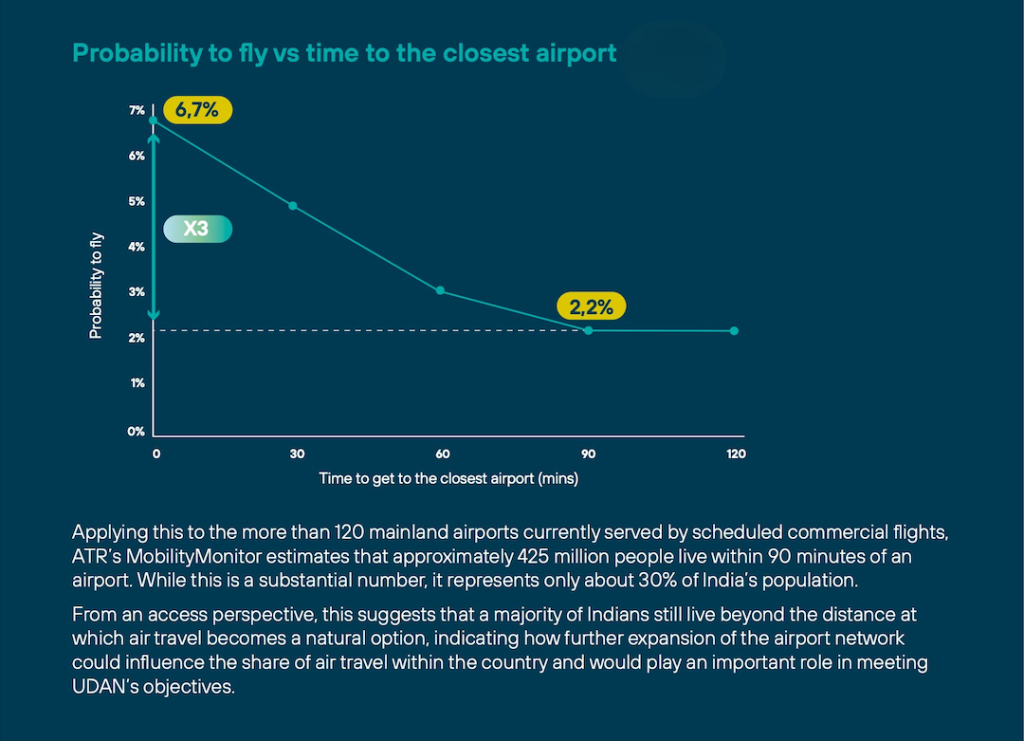

These insights are drawn from ATR’s MobilityMonitor, a mobility analysis platform developed by ATR to examine how people actually travel across India. Based on anonymous, multimodal journey data, the MobilityMonitor allows ATR to assess total inter‑city mobility, the current share of air travel, and where latent demand already exists beyond today’s air network.

One of the most persistent misconceptions about regional aviation in India is that demand must be created. In reality, the demand is already there. Millions of trips take place every day between non-metro cities, primarily by road and rail.

What aviation lacks is share.

According to ATR’s MobilityMonitor analysis, regional air travel today accounts for only around 2–3 per cent of domestic mobility in India. In more mature aviation markets, that figure is closer to 8–9 per cent. The gap does not reflect a lack of travel; it reflects aviation’s limited ability to offer a competitive alternative on short distances.

Data reinforces this point. Nearly 90 per cent of domestic trips in India occur on routes below 400 nautical miles. These are distances where air travel can deliver meaningful time savings—but only if the economics allow fares to remain close enough to surface transport to justify a modal shift.

This is where turboprops enter the picture.

As Jean-Pierre Clercin, Head APAC, ATR, puts it, “Growth in regional aviation will come from increasing aviation’s share of existing demand, rather than creating demand from scratch.” That distinction matters because it places economics—not aspiration—at the centre of the discussion.

Short routes demand a different aircraft logic

Short-haul regional routes behave very differently from longer trunk sectors. Load factors are more volatile, yields are tighter, and route viability depends heavily on frequency rather than aircraft size.

Attempting to operate these routes with aircraft optimised for longer sectors introduces risk.

Larger aircraft require higher load factors to break even. Longer stage-length economics do not always translate well to sectors under an hour.

Turboprops, by contrast, are designed around exactly these constraints. Lower fuel burn at short distances, competitive cost per available seat kilometre (CASK), and the ability to sustain frequency without excessive capacity make them structurally better suited to regional networks.

The risk profile matters as much as the cost profile. Opening a new short-haul route between two secondary cities is fundamentally different from launching a thin long-haul service. Shorter routes allow airlines to test markets, adjust schedules, and build connectivity incrementally.

This logic also explains why many regional passengers in India still find themselves routing through major hubs to travel between nearby cities. The network has historically been designed around aircraft and economics that favour consolidation, not dispersion.

Network design, not just airport count

India has invested heavily in expanding its airport footprint, particularly under the UDAN programme. But airport availability alone does not guarantee connectivity. Aircraft choice determines whether those airports can be integrated into viable networks.

From a network-design perspective, regional connectivity works best when built around short first-leg routes that link smaller cities into the wider system. These dense short-haul connections make networks easier to sustain, while longer routes develop more selectively.

This model depends on aircraft that can operate short legs profitably, turn quickly, and maintain frequency without excessive cost exposure. Turboprops fit that requirement more naturally than alternatives designed for longer, higher-speed missions.

Analytical tools such as ATR’s MobilityMonitor, which combines origin-destination modelling and time-value analysis across all transport modes, increasingly reinforce this view. The question is not whether demand exists on the ground, but whether aviation can save enough time, at low enough cost, to justify switching modes.

Affordability remains the critical lever. Ground transport in India is inexpensive. Aviation does not need to match those fares, but it must remain close enough that passengers see value in paying a modest premium for speed and reliability. Turboprop economics make that equation easier to balance.

What global regional markets reveal

International experience offers further evidence that regional aviation success is closely tied to turboprop operations—though no single market is directly comparable to India.

In New Zealand, low population density and dispersed communities make surface infrastructure expensive to scale. Regional aviation plays a central role, supported by turboprop fleets optimised for short sectors.

Japan presents a different geography but a similar outcome. As an archipelago, physical constraints limit ground connectivity. Aviation fills those gaps, particularly on regional routes where turboprops remain competitive despite the presence of high-speed rail elsewhere.

Brazil is often cited as one of the strongest turboprop reference markets globally. Long distances, uneven infrastructure, and a large number of secondary cities have sustained regional turboprop operations for decades.

Indonesia, too, relies heavily on aviation to overcome geographic fragmentation, with turboprops forming the backbone of many regional networks despite economic constraints.

What these markets share is not uniform demand, but a reliance on aircraft that can make short-haul economics work reliably. Where ground transport is inefficient or prohibitively expensive to expand, turboprops become the default solution.

India increasingly shares those characteristics as connectivity spreads beyond major metros.

Why adoption has been uneven

Despite policy intent and initiatives such as UDAN, regional aviation growth has not been uniform across operators.

For smaller and start-up airlines, access to affordable capital was a constraint for years. That situation is beginning to change. Equity interest and financing appetite have increased, supported in part by clearer policy signals and maturing airport infrastructure.

Larger airlines face a different set of priorities. Fleet expansion, narrowbody inductions, and long-haul growth dominate near-term planning. Regional flying, while strategically relevant, often competes for attention and resources with higher-profile network expansion decisions.

This divergence explains why momentum in turboprop operations is often strongest among newer or regionally focused players, while larger carriers move more cautiously. The economics of turboprops may align well with regional demand, but fleet strategy and capital allocation still determine how quickly that alignment translates into scale.

Charter flying: a limited but relevant niche

Charter and premium regional flying is frequently discussed as a complementary opportunity, but here too, turboprop economics define the limits.

Globally, such operations are typically driven by high-net-worth individuals and leisure travel to resorts or remote destinations. Traditional corporate shuttle flying is often a smaller component than assumed.

In the United States, operators such as JSX have demonstrated that secondary airports and fixed-base operators can support point-to-point flying without relying on major hubs. These services succeed by reducing travel friction—shorter ground times, simpler terminals, and faster end-to-end journeys—rather than by deploying large aircraft or high capacity.

Whether similar models can scale in India remains uncertain. Demand patterns, willingness to pay, and supporting infrastructure differ significantly. As Clercin notes, “There is demand for granular, city-pair connectivity when it removes friction from the journey. Whether that can be directly transposed to India is still an open question.”

Where charter flying does emerge, turboprops are often better positioned than larger aircraft to keep costs contained while offering flexibility.

Sustainability strengthens the turboprop case

Sustainability considerations further reinforce the turboprop argument.

Sustainable Aviation Fuel (SAF) is increasingly viewed as the most credible near-term pathway to emissions reduction.

Turboprops, with lower baseline fuel burn on short sectors, stand to benefit disproportionately from SAF adoption.

Hybrid-electric and electric propulsion concepts continue to evolve, but economics remain decisive. Lower energy costs alone do not offset higher acquisition and maintenance costs today. For regional aviation to compete with cars and buses, cost discipline matters as much as innovation.

Clercin argues that “The test for new propulsion concepts is not novelty, but whether they can reduce ownership and operating costs enough to compete with surface transport: If you want to compete against the car and the bus, you better be sharp on those economics.”

A structural, aircraft-led transition

India’s regional aviation opportunity is not speculative. It is structural.

ATR’s MobilityMonitor shows that the demand already exists. The airports are expanding. Policy intent is clear. What remains is aligning aircraft economics with the realities of short-haul travel.

That alignment narrows the field. Aircraft designed for longer sectors or higher speeds struggle to deliver frequency and affordability without increasing risk. Turboprops, by contrast, are purpose-built for the problem India is trying to solve.

The next phase of regional aviation growth, therefore, will not be defined by ambition alone, but by whether networks are built around aircraft that make short routes work—consistently, affordably, and at scale.

Also Read: India’s Regional Mobility Boom Points Clearly to Turboprops