- IndiGo and Adani Airport Holdings have linked the BluChip loyalty programme with duty-free shopping across AAHL airports, introducing one of the first airline–airport retail loyalty integrations in India and bringing airline loyalty into the airport commercial ecosystem.

- Global examples from Dubai, Doha and Heathrow show that loyalty-linked retail can increase duty-free spending and engagement; India’s relatively low duty-free conversion rates suggest significant room for growth if the model is executed well.

- The partnership highlights a broader shift in airport economics toward stronger non-aeronautical revenue, but its success will depend on visibility within the travel journey, smooth fulfilment at the airport, and the ability to extend loyalty engagement beyond flight bookings.

India’s largest airline and the country’s largest private airport operator have quietly done something that has no real precedent in Indian aviation.

When IndiGo and Adani Airport Holdings Limited (AAHL) announced on 16 March 2026 that IndiGo BluChip members can now earn loyalty points on duty-free shopping at AAHL-managed airports, it may have looked like a routine loyalty extension. It is anything but.

The mechanics are simple: five BluChips for every ₹100 spent on duty-free products pre-booked through Adani’s digital platform, with convenient pickup at the airport.

But behind that earn rate lies a much larger strategic bet — on India’s travel retail opportunity, on airport commercial transformation, and on the long-term value of a frequent flyer programme that, just over a year after launch, has already crossed seven million members.

India’s First Airline-Airport Loyalty Integration

To understand why this partnership matters, we need to start with where Indian airports stand commercially. Airport revenues globally come from two broad buckets: aeronautical charges (landing fees, parking, terminal charges) and non-aeronautical income (retail, duty-free, food and beverage, lounges, advertising, and real estate).

At the world’s leading hub airports, non-aeronautical revenues — from retail, duty-free, F&B, parking, and real estate — typically account for between 40% and 50% of total income, with Middle Eastern airports leading the range.

At most of AAHL’s airports, that ratio has historically leaned heavily toward aeronautical charges, with non-aero playing a secondary role. Mumbai has been the exception, operating closer to a 50-50 split. Across the network, non-aeronautical revenue now accounts for approximately 54% of total income — a meaningful improvement, but still short of where AAHL wants to be.

The company has publicly committed to growing that share to 70% by 2030, backed by a ₹20,000 crore city-side development plan spanning retail, hospitality, and commercial real estate across its airports.

IndiGo BluChip, launched in November 2024, had enrolled over two million members within months of launch and crossed seven million by late 2025.

That is an enormous and fast-growing loyalty base for a relatively young programme — and one built almost entirely on the back of IndiGo’s domestic dominance: over 2,000 daily flights, 140+ destinations, and 124 million customers carried in CY2025.

The partnership essentially puts that loyalty base to work inside an airport commercial ecosystem that AAHL desperately needs to monetise. Both sides have a clear, shared incentive, and that structural alignment is why this tie-up deserves serious attention.

Photo: CSMIA

No other Indian carrier has formally integrated its Frequent Flyer Program (FFP) into an airport operator’s duty-free and e-commerce ecosystem at this scale.

Air India’s Maharaja Club exists, but it has no published partnership with airport retail infrastructure in India. The IndiGo–Adani deal is, by any fair reading, the first of its kind in the Indian market.

Globally, the Playbook Already Exists — and It Works

What IndiGo and Adani have built is not a new idea globally. The world’s leading carriers integrated their loyalty programmes with airport duty-free years ago, and the results have shaped how airports and airlines think about commercial partnerships.

Emirates Skywards and Dubai Duty Free (DDF) represent perhaps the most advanced version of this model. Members can redeem miles directly at DDF’s point of sale — 4,000 miles for AED 75 — making the loyalty currency genuinely spendable at the airport shop, not just on flights. DDF generates over $2 billion in annual sales; the Emirates partnership is widely credited with driving impulse purchases and loyalty-linked footfall at Dubai airports. Redemption, not just earning, is the hook.

Etihad Guest and Heinemann Duty Free took a similar earn-at-retail approach to the one IndiGo–Adani is now replicating: one Etihad Guest Mile per euro spent across Heinemann shops at airports in Europe, Australia, Indonesia, and Singapore. The design is clean — swipe your FFP card, earn miles, no complexity. Heinemann pays Etihad for the miles at a bulk rate; Etihad books high-margin partner revenue; the duty-free retailer treats it as a marketing cost that drives incremental basket and footfall.

British Airways Executive Club members earn Avios at World Duty Free outlets across outlets at London Heathrow — one Avios per pound or euro, with 250 bonus Avios on the first linked purchase. The partnership, run through the Club Avolta/Dufry app, also allows members to spend Avios at 0.5p per Avios — making it a genuine earn-and-burn model, not just an earn one. Earn is capped at 3,000 Avios per transaction. An identical offer exists for Iberia Plus members at Spain Duty Free stores.

Air France-KLM’s Flying Blue members earn three miles per euro at Aelia Duty Free stores in France. Qatar Airways Privilege Club members earn and redeem Avios at Qatar Duty Free at Doha. Frankfurt Airport, one of Europe’s busiest hubs, has embedded Lufthansa’s Miles & More programme across more than 60 outlets at the airport — duty-free, F&B, parking, and more — creating what is effectively a whole-of-airport earn ecosystem anchored to the home carrier’s FFP.

IndiGo–Adani’s earn rate of five BluChips per ₹100, with each BluChip carrying an official redemption value of ₹1 against flight bookings, though realised value can vary by route and availability, is comparable in spirit to these programmes.

What it currently lacks is the redemption dimension — the ability to pay with BluChips at duty-free checkout, as Emirates enables with miles at DDF and as British Airways now allows at Heathrow. That will likely be the natural evolution of the programme. For now, it earns, not burns, and the design is intentionally frictionless: browse, pre-order, pay online, collect at the airport via QR validation.

What the Numbers Say About the Opportunity — and the Risks

The commercial logic rests on three things: India’s travel retail headroom, the behavioural economics of airport shopping, and the structural economics of loyalty programmes.

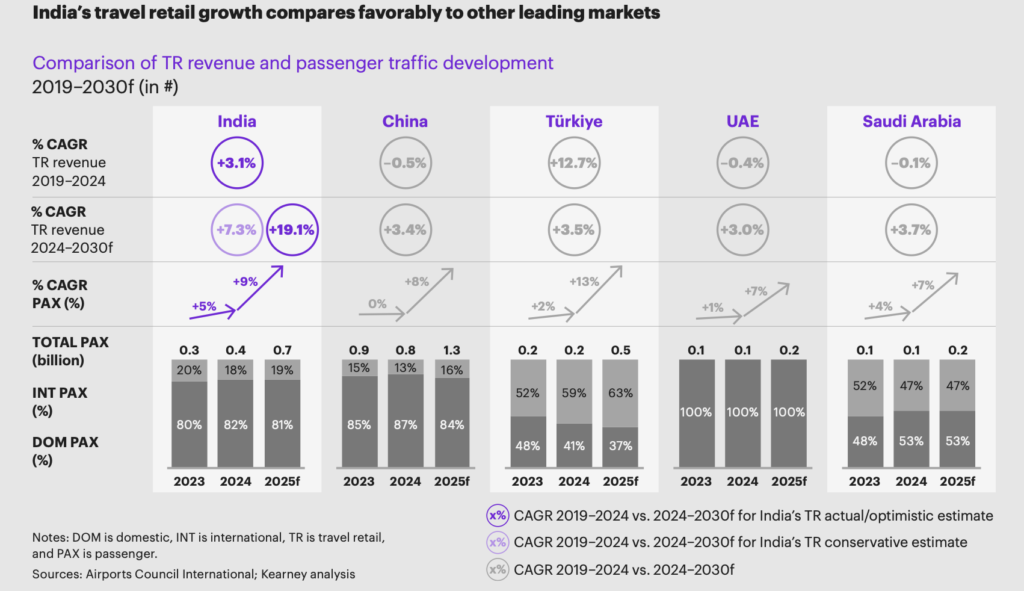

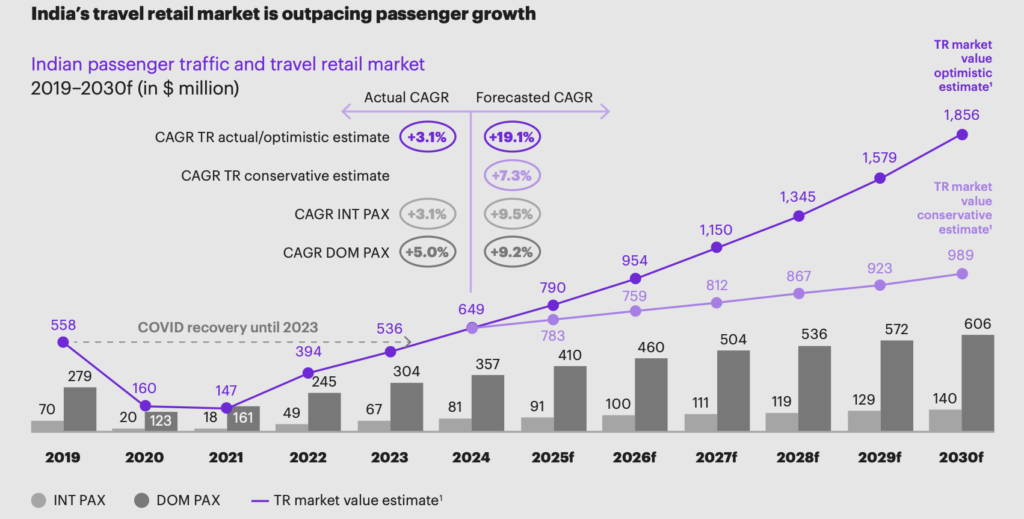

On the market size, Kearney’s travel retail report (developed with TFWA) is the clearest data point: India’s travel retail market is expected to reach nearly $1 billion by 2030 in a conservative scenario (7.3% CAGR), and up to $1.8 billion annually in an optimistic one (up to 19% CAGR). India is on track to become the world’s third-largest air travel market by 2030, with passenger traffic growing at 9% CAGR to over 745 million annually. Average monthly per capita travel retail spending has already more than doubled — from $29 in 2019 to $62 in 2024.

Yet despite this, India’s duty-free conversion is strikingly low — estimated at roughly 5% average across airports, with 8–10% at the top international gateways. Compare that with 15% in Dubai and around 25% in Istanbul, and the gap becomes an opportunity. If IndiGo–Adani can nudge conversion even a few percentage points higher at Mumbai, Ahmedabad, or Thiruvananthapuram — cities from which international traffic is meaningful and growing — the incremental revenue impact at scale is real.

Airport retail research is equally instructive about what actually drives purchases. An Airports Council International (ACI) Asia-Pacific and Middle East travel retail study is direct on this: approximately 70% of buying decisions remain impulse-driven. Product choice (39%) and pricing/promotions (29%) together explain nearly 70% of purchase motivation.

Convenience and time efficiency rank ahead of ambience. The same study, however, notes that while digital engagement is growing, it is “currently driving only 2% of additional sales.” That is a calibrating number. It means the partnership, by itself, is not a guarantee of transformation. What it does is add a meaningful incentive (BluChips) onto a pre-order and convenience layer — addressing precisely the three levers the research identifies: price/promotion perception, reduced time pressure, and planned purchase. The design is directionally right; execution will determine scale.

On loyalty programme economics, the global evidence is unambiguous. Airlines have turned FFPs into high-margin revenue engines not primarily through flight redemptions but through partner-mile sales. Delta’s American Express co-brand partnership is estimated to generate around $7 billion annually for the airline — one of the largest commercial partnerships in global aviation.

Even for smaller partners like airport retailers, the model is clear: the airport or retailer buys miles or points in bulk from the airline at a fixed rate (typically 1–2 cents per mile globally), awards them to shoppers, and treats the cost as a marketing and customer acquisition expense. The airline books this as near-pure revenue. For IndiGo, with seven million BluChip members and 124 million annual passengers, selling BluChips to AAHL is a commercial lever that adds revenue without adding a seat or a flight.

There are also structural risks worth naming. IndiGo is, first and foremost, a domestic LCC. The vast majority of its passengers fly within India and are not duty-free eligible. The partnership’s commercial impact is therefore concentrated on a subset of travellers — international departures and arrivals — who happen to fly IndiGo and hold active BluChip accounts.

Effective segmentation and targeting — surfacing the offer in the booking flow, in pre-departure communications, and in the app, not just in a partner listing — will determine whether the partnership reaches its potential or stays a feature for a small minority of members.

Airport retail research using transaction data from Incheon International Airport has also shown that while LCC passengers can have comparable or even higher duty-free purchasing power than full-service travellers, poor terminal environments and service friction can significantly suppress sales. The fulfilment experience — pick-up queues, QR validation, inventory availability — matters as much as the loyalty mechanic.

Can This Model Scale? What It Means for Indian Aviation

The more interesting question is not whether IndiGo–Adani works, but whether it catalyses a broader shift in how Indian airports and airlines think about commercial partnerships.

India has approximately 157 operational airports; 14 are run on public-private partnership models, with the number growing. GMR Airports (Delhi, Hyderabad, and Goa), the Airports Authority of India, and BIAL (Bangalore International Airport Limited) in Bengaluru all operate significant duty-free and retail ecosystems. Bengaluru Airport launched its own campus loyalty programme, Pulse Rewards, in 2025, covering duty-free, F&B, and retail across the airport. None of these, however, are formally linked to an airline FFP in the way IndiGo–Adani now is.

IndiGo could, in theory, replicate this model with other airport operators. Air India and its Maharaja Club could pursue similar partnerships at GMR-operated airports or at BIAL. Akasa Air, which has also been building its loyalty ecosystem, could become a candidate as it scales.

Even from AAHL’s side, adding a second or third airline FFP to the duty-free earn ecosystem — the way Frankfurt’s non-aero retail accepts Miles & More from multiple Lufthansa Group carriers — would deepen the commercial impact. The runway for replication is wide.

The Kearney report frames the structural opportunity with precision: India’s travel retail growth will require coordinated action from what it calls a “pentarchy” — governments, airport operators, airlines, retailers, and brands — acting together.

The IndiGo–Adani partnership is, in its current form, a bilateral link between two of those five. The further it expands — to more airports, more earn occasions, and eventually to redemption at the point of sale — the closer it moves toward what the best global examples have already achieved.

AAHL’s stated ambition to move its non-aero revenue share toward 70% is not achievable through passenger volume growth alone. In FY2024-25, the company posted revenue of ₹10,224 crore — up 27% year-on-year, while serving 94.4 million passengers across its seven operational airports. The growth is impressive; the commercial mix transformation still lies ahead. The non-aero transformation requires changing passenger behaviour, not just counting more of them.

Loyalty-linked retail is one of the most consistently effective tools airports and airlines use globally for doing exactly that — increasing dwell time, conversion rates, and basket size simultaneously. Studies suggest that a 10% increase in dwell time correlates with approximately a 5% rise in non-aeronautical revenues.

For IndiGo, the logic is slightly different but equally compelling. A loyalty programme that only rewards flying is a loyalty programme that passengers forget between trips. BluChip members who earn points on a pre-ordered bottle of Scotch or a cosmetics purchase at Mumbai airport are engaging with the IndiGo brand at the airport, not simply through a discounted. That kind of touchpoint — low-effort, high-frequency, reinforcing — is precisely what builds the habitual relationship between a traveller and an airline that transcends price comparison.

India’s travel retail consumers are also increasingly younger: the ACI study highlights that Gen Z and Millennials spend 3.5 times more at airport retail than Gen X and Boomers combined, and this cohort is already comfortable with digital pre-order, mobile payments, and click-and-collect. IndiGo’s demographic and IndiGo’s opportunity are converging at exactly the right time.

The partnership is already active at six airports today. Guwahati and Navi Mumbai are next. The architecture is in place. Whether this becomes India’s version of the Emirates–Dubai Duty Free model — or remains a modest loyalty footnote — will depend on execution: visibility, ease of pick-up, and how quickly BluChips move from earning to spending at the airport.

Also Read: How the Airports Authority of India is Expanding Aviation Infrastructure